The Business Manager Visa is a residence status granted to foreign nationals who reside in Japan for the purpose of managing or operating a business.

Due to the ministerial ordinance revision in October 2025, the requirements for obtaining a Business Manager Visa have been significantly tightened. The business scale requirement, once known as a “¥5 million investment,” has now been raised in principle to “an investment of at least ¥30 million.”

For those establishing a company for the first time, preparing ¥30 million solely from personal funds is an extremely high hurdle. In such cases, is it acceptable to secure this capital through loans (borrowings) or gifts (financial support) from family members? This page provides an explanation of investment requirements and funding methods for the Business Manager Visa under the new criteria.

Is the ¥30 Million Investment Absolutely Required?

Before discussing funding methods, the fundamental question is whether a ¥30 million investment is absolutely necessary. In conclusion, under the new standards, an investment (or business scale) of ¥30 million is generally mandatory.

Under the previous rules, applicants only needed to meet either “an investment of ¥5 million” or “employment of at least two full-time staff members.” However, under the revised standards, all of the following requirements must now be satisfied:

- The amount of stated capital or total investment must be at least ¥30 million

- At least one full-time employee must be engaged in the business

- The applicant or a full-time employee must have a certain level of Japanese language proficiency (equivalent to JLPT N2 or higher)

In other words, the previous option of “hiring employees instead of investing funds” is no longer available. Both “¥30 million in capital” and “employment of personnel” are now required.

Therefore, for those applying for a Business Manager Visa going forward, securing funds on the scale of ¥30 million is an unavoidable challenge.

Can the Investment Be Funded by Loans or Gifts?

In conclusion, preparing part or all of the investment funds through loans (borrowings) or gifts (financial support) from others is not prohibited by law.

However, with the threshold raised from ¥5 million to ¥30 million, the level of scrutiny is now far stricter than before.

It is not sufficient to simply have ¥30 million in a bank account; whether the source of funds is legitimate will be rigorously examined. Depending on the funding method, careful attention must be paid to the following points.

Key Point 1: Strict Elimination of “Temporary Funds” and Immigration Interpretation

The most critical issue is the suspicion of “temporary funds” (misegane).

Borrowing money temporarily just to deposit it into an account at the time of the visa application, and then repaying it immediately after approval, constitutes a false application and must never be done.

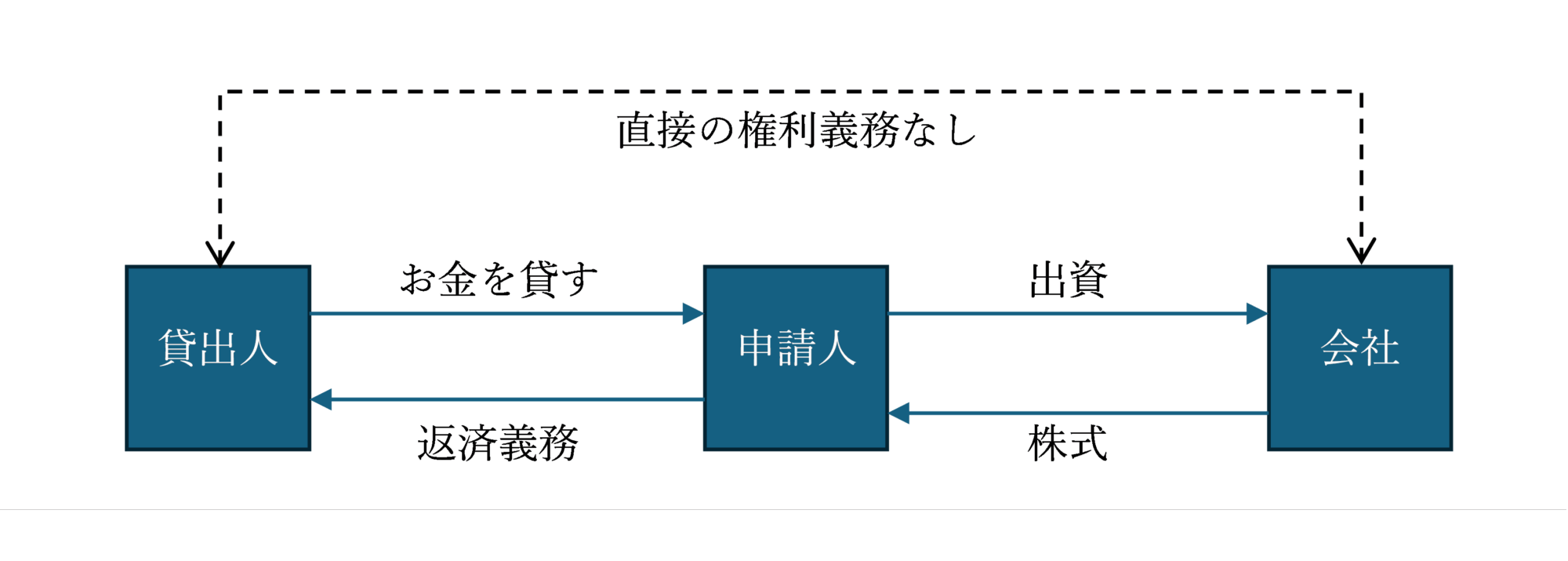

There is also an important practical consideration. If a founder borrows money from a third party and uses those funds as capital, the Immigration Services Agency’s “Guidelines for Examination of Entry and Residence” explicitly state that “using borrowed funds with a repayment obligation as capital is considered illegal.”

However, the original legal interpretation under the Companies Act is different.

Companies Act (Excerpt)

(Liability in Cases of Fictitious Contribution)

Article 52-2 In the cases listed in the following items, the incorporator shall be obligated to perform the acts specified in each item toward the stock company.

(i) Where payment under Article 34, paragraph (1) is fictitious: payment of the full amount related to the fictitious contribution

(omitted)

Originally, if individual A borrows money from third party B and invests it into Company C to acquire shares, the repayment obligation lies with A. Company C has no obligation to B. Even if A loses the ability to repay, the outcome is merely that A’s ownership rights in Company C may ultimately be transferred to B; Company C itself is not obligated to repay B directly from its own funds.

In other words, the immigration authority’s interpretation that “investment using borrowed funds is illegal” is legally questionable. However, since this interpretation is stated in the examination guidelines, actual screening is conducted based on the administrative authority’s view. Challenging this interpretation would require litigation, which could take over five years if pursued up to the Supreme Court.

As a result, although investing borrowed funds is legally permissible, in practice it is extremely difficult to obtain a Business Manager Visa using such funds.

Key Point 2: Gifts (Financial Support) — Japanese Gift Tax and Overseas Transfers

If financial support is received from relatives as a “gift” without repayment obligation, there is no need for a repayment plan as with loans. However, this instead raises the issue of gift tax.

If a person receives a gift of assets within Japan, the recipient is subject to Japanese gift tax. In the case of a ¥30 million gift, the tax rate is extremely high (up to over 50%), meaning that a substantial portion of the startup funds could be lost to taxation.

To avoid this, it is strongly recommended that “the transfer of gifted funds be conducted outside Japan”.

Special Rule for Those Who Have Resided in Japan for Less Than 10 Years

Under Japanese tax law, even if a foreign national has a residence in Japan, if their total period of stay in Japan within the past 15 years is 10 years or less (i.e., a temporary resident), gifts of assets located outside Japan are not subject to Japanese gift tax (subject to certain conditions, such as the donor also being a foreign national).

In other words, if funds are directly transferred from parents into a bank account in Japan, it may be considered a “domestic asset gift” and subject to taxation. However, if the transfer is made from the parent’s overseas account to the applicant’s overseas account (i.e., a gift made outside Japan), and then brought into Japan as the applicant’s own funds, Japanese gift tax will not apply.

When receiving financial support, it is advisable to consult a tax professional in advance regarding the transfer route and timing.

Conclusion

Following the 2025 revision, obtaining a Business Manager Visa has become significantly more difficult. Preparing ¥30 million in capital requires comprehensive planning, including proper documentation of fund transfers and compliance with tax regulations.

Proceeding without professional guidance may lead to insufficient explanation of fund sources or unexpected tax risks. For company establishment and visa applications under the new requirements, it is strongly recommended to consult a specialist familiar with the latest legal revisions and practical procedures.